Case 01

Remote Farm Verification

Confirm mapped borrower fields, crop type, field size, and season status before disbursement or restructuring.

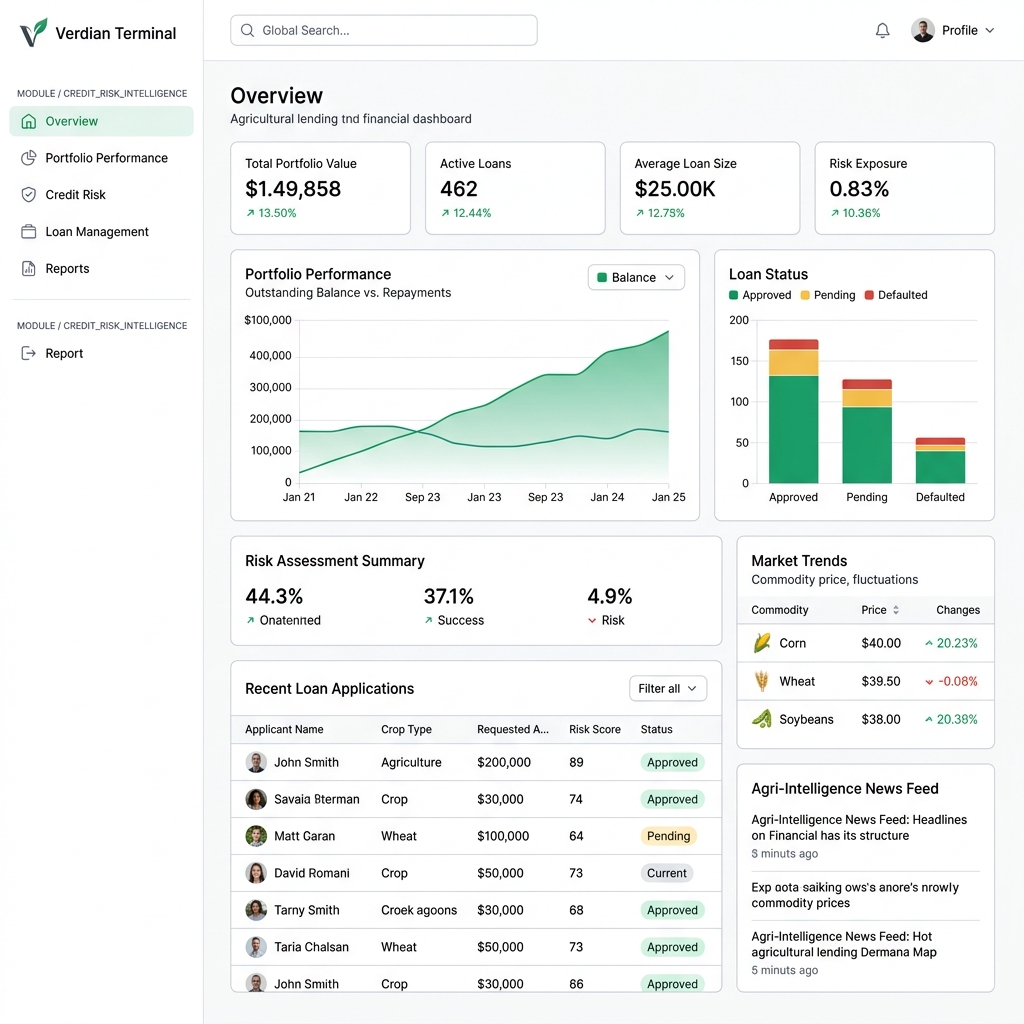

Verify borrower farms, monitor crop stress, and turn field evidence into credit decisions, Verdian Score movement, and committee-ready loan files.

Exposure

Mapped loan collateral

Repayment Risk

Crop stress alerts

Verdian Score

0-1000 risk signal

Credit Files

Committee-ready packs

Verdian translates field observations into borrower verification, portfolio monitoring, risk movement, and evidence that can travel into a loan file.

Confirm mapped borrower fields, crop type, field size, and season status before disbursement or restructuring.

Track financed fields through the season with optical, radar, weather, and field-level coverage quality signals.

Prioritize accounts where vegetation decline, moisture stress, or weather shocks are likely to affect repayment.

Generate auditable Credit Committee Packs with field evidence, Verdian Score, PD, exposure caps, and policy constraints.

Field Evidence

Satellite, radar, weather, yield confidence, and borrower activity in one credit record.

Each financed field becomes a verified digital asset with crop, farmer, farm, and boundary context.

Verdian detects stress, cloud-adjusted observation quality, yield confidence, and management signals while the season is still in progress.

The 0-1000 Verdian Score converts agronomic performance and compliance evidence into a lender-readable risk signal.

Risk teams can prioritize field visits, restructure exposure, request evidence, or escalate accounts before repayment risk becomes arrears.

Verdian converts agronomic uncertainty into lender-readable evidence for origination, monitoring, renewals, collections, and portfolio review.

Agronomic performance and borrower evidence in a consistent score scale.

Field condition, yield confidence, economic viability, and stress movement.

Optical imagery, SAR radar, weather, and field coverage quality controls.

Requested amount, exposure caps, haircut rules, and binding constraints.

Rank borrower accounts by crop stress, repayment risk, and action urgency.

Credit Committee Packs and data trails that can be reviewed by risk teams.

Commercial banks financing row crops and horticulture

Microfinance institutions lending to smallholders

Input suppliers offering seasonal credit

Insurers and reinsurers monitoring agricultural exposure

Development finance teams funding climate-smart agriculture

Agribusiness aggregators financing production contracts

Verdian gives lenders field-level evidence for borrower verification, crop performance monitoring, early stress detection, and credit committee review. The goal is not to replace underwriting, but to make agricultural exposure visible while there is still time to act.

The Verdian Score is a 0-1000 agricultural performance and risk signal. It combines satellite observations, field evidence, weather exposure, yield confidence, and borrower activity into a lender-readable score.

Yes. A lender can start by mapping an active portfolio, linking fields to borrowers, and monitoring risk movement during the season before expanding into origination, renewals, and collections workflows.

Verdian is built around credit risk workflows. The output is portfolio monitoring, loan evidence, default-risk signals, and committee-ready documentation rather than general farm management advice.

Start with an active portfolio, map borrower fields, and use Verdian to monitor agricultural credit risk through the season.